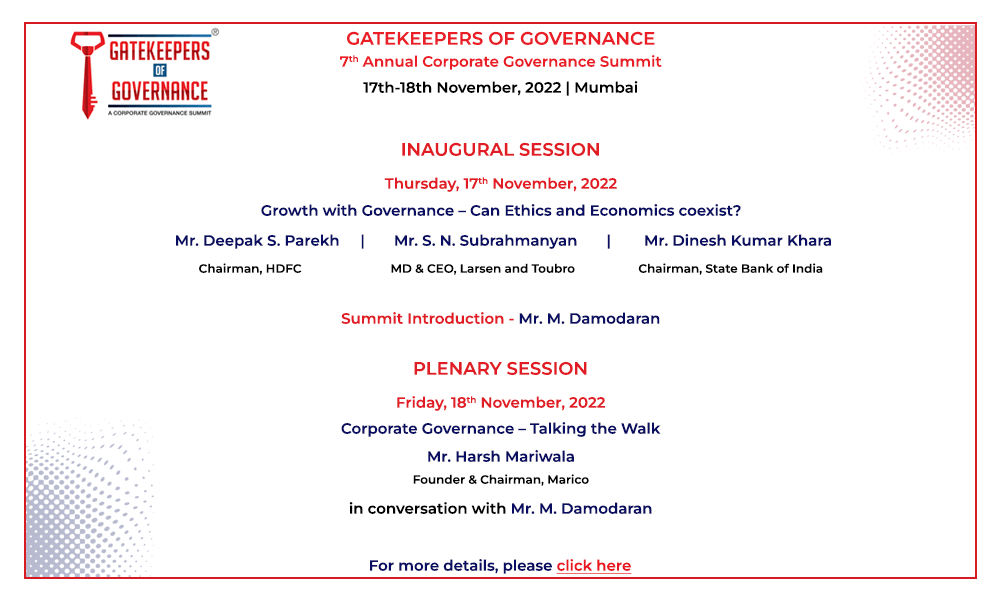

We were privileged to organise the 7th Gatekeepers of Governance Annual Corporate Governance Summit on 17-18 November 2022. A report will be published shortly.

In its latest consultation paper (there has been a steady stream of consultation papers) on review of disclosure requirements for material events or information under SEBI LODR Regulations, 2015 (LODR Regulations), SEBI has sought to comprehensively identify every possible material event or information, and to standardise the manner in which such information is to be disclosed.

Securities market regulation envisages a disclosure-based regime, which mandates that all relevant information ought to be made available to stakeholders, without delay, so that they can take informed investment decisions. The consultation paper under reference, has been triggered by the “many complaints/ references regarding inadequate/ inaccurate/ misleading/ delayed disclosures” made by listed entities.

Every such effort invites both bouquets and brickbats. Let us begin with the bouquets. This is as detailed and comprehensive an exercise as can be attempted. While making out a case for more disclosures, faster disclosures, and timely disclosures, the need for confidentiality in some matters has not been lost sight of. Further, it also takes into account the speed at which information is disseminated in this digital age, and addresses the need to reduce some timelines which were prescribed in a non-digital context. The desire of listed entities for uniformity in determining materiality of events or information has also been taken on board.

Some aspects of the consultation paper merit specific comments. They have been detailed in the following paragraphs.

Materiality threshold – In para 3.1.6, the threshold value or the expected impact in terms of value has been laid down in terms of percentages of the turnover, the net worth, or the 3 year average of absolute value of profit/ loss after tax. The lowest of these will constitute the materiality threshold. While this approach brings quantitative uniformity in regard to disclosures, it does not address the possibility that there could be an event or information below this threshold which could, by impacting the reputation of the company, be deemed material.

Materiality policy – In para 3.2.3, it has been specifically stated that the materiality policy of the listed entity shall not dilute any requirements specified under Clause (ii) of Regulation 30(4) of LODR Regulations. The next sub-paragraph states that the materiality policy shall be framed in a manner so as to assist employees in identifying a potentially material event or information, which shall be escalated and reported to the relevant Key Managerial Personnel (KMP) for determining materiality. If the employee concerned identifies a potential material event or information in terms of the thresholds, there need not be a requirement for the relevant KMP to further determine materiality, since objective criteria will form the basis for such determination.

Timeline for disclosure: In para 3.3.3, it has been proposed that for material events or information which emanate from the listed entity, the timeline for disclosure by the entity shall be reduced from 24 hours to 12 hours. This reduction of the timeline has been recommended because in the present age of digital communication, and widespread usage of social media, information gets disseminated very quickly. It is not understood how the proposed reduction from 24 hours to 12 hours will adequately address the problem. This would seem to be a recommendation in the nature of tokenism, rather than a sufficiently strong move to promote timely disclosures.

In para 3.3.4, it has been provided that events or information which emanate from a decision taken in a meeting of the Board of Directors, shall be made within 30 minutes from the closure of such meeting. Some meetings last for several hours, and the material event or information might have been decided in the early part of the meeting. Ideally, the disclosure should be within 30 minutes of the decision being taken, rather than 30 minutes from the closure of the meeting.

Verification of market rumours – This is one subject on which significant changes have been suggested. Regulation 30(11) of LODR Regulations provides that a listed entity may, on its own initiative, confirm or deny any reported event or information to the Stock Exchanges. It is now proposed that the top 250 listed entities shall “necessarily confirm or deny any event or information (emphasis supplied) reported in the mainstream media, whether in print or digital mode, which may have material effect on the listed entity.” Regrettably, many news items, in the mainstream media, neither pertain to any event, nor to any information. There are purely speculative reports, of a sensational nature, and on occasion, driven by the agenda of some person or institution, which find their way to the mainstream media. If a listed entity is to respond to all such newspaper reports, they could end up doing just that, and not transacting the business for which the entity was set up. This recommendation is clearly excessive, and should not be followed up.

Disclosure of communication from regulatory, statutory, enforcement or judicial authority – In para 3.5.2, it has been observed that some of these communications may contain confidential information, or may have regulatory restriction on disclosure. To SEBI’s credit, it has been acknowledged that companies would find it a challenge to make such disclosures upfront (emphasis supplied). What has been suggested is that a provision may be added in Regulation 30, enabling SEBI to come out with guidance for disclosure of such communications. This is more easily said than done. While companies are not expected to make upfront disclosures of such communications, there would be several different situations for deciding the appropriate time for such disclosures. It could be somewhat difficult to capture all of these in a single guidance note. While attempting a guidance note, SEBI should be mindful of the fact that premature disclosures can adversely affect a company and its stakeholders.

In events proposed to be added in Para A of Part A of Schedule III of LODR Regulations, it has been correctly acknowledged that it would be impractical to expect investors to keep track of all the announcements and communications made by the listed entity, or its officials, from time to time, and through different media fora. The fact that this could result in information asymmetry has been rightly taken note of. The solution suggested in para 3.7.2 is that all such announcements and communications should be disclosed at a single place. The logical place for disclosure of material information is the website of the Stock Exchange where the company is listed. Given the wide variety of stakeholders, and the fact that not all of them routinely access the websites of the companies and the Stock Exchanges, such disclosure itself could lead to information asymmetry. Disclosure on a Stock Exchange is like a publication in the official gazette, where there is a presumption that everyone has taken note of what has been stated in the communication. It will be interesting to ascertain what percentage of shareholders routinely access the websites of the Stock Exchanges.

One way to address the problem, and this is for companies, and not for the Regulator, is to discourage the practice of company officials, authorised and unauthorised, from making off the cuff remarks, either on their own, or in response to questions from the media. It would be useful for companies to have designated spokespersons who are trained in communicating with the media, and to ensure that only they make statements and announcements relating to the company.

In para 3.7.3, the suggested disclosure relates to developments such as suspension, imposition of fines/ penalties, settlement proceedings, debarment, disqualification, closure of operations, sanctions imposed, warning or caution, search or seizure, inspection, investigation into the affairs of the entity and reopening of accounts. The problem with indicating a long list of specific developments is that something could be missed, and therefore, by necessary implication, will not be disclosed. A better formulation, which is crisp and concise, should be attempted.

In para 3.7.5, it has been suggested that in the case of resignation of a KMP, or a Senior Management Personnel (SMP), or a Director, other than Independent Director, the letter of resignation, along with the detailed reason for resignation, shall be disclosed to the Stock Exchanges, within 7 days from the date of resignation. In a recent case, the news of the resignation of a KMP from a listed entity came out 2 days before the resignation took effect. It is not known how such possibilities, rare as they might be, will get appropriately addressed.

The consultation paper also makes a number of recommendations regarding disclosures covered under Para B of Part A of Schedule III of LODR Regulations. In Para 3.10.3, it has been noted that loan agreements for lending to wholly owned subsidiaries of the listed entity may not be material, and would usually be in the normal course of business. This amounts to giving an easy pass to companies that use subsidiaries for colourable purposes.

Disclosure of cyber security incidents – Para 3.11.2 notes that immediate disclosure of such events may not be desired since the entity may be vulnerable to further attacks. The suggestion therefore is that after root cause analysis is done, and remedial measures are taken, an appropriate disclosure should be made in the quarterly compliance report on Corporate Governance. This could give rise to the possibility that such incidents could get reported in the media, and could lead to speculation, for want of an authentic statement from the company. An appropriately worded statement, disclosed as soon as the event takes place, could be the preferable option.

Briefly stated, the consultation paper provides for a lot of additional disclosures, within a shorter timeframe, and with more details than had been mandated in the past. It is fair to ask whether corporates should contemplate setting up a separate department for disclosures with a Chief Disclosure Officer.

Sunlight is the best disinfectant, but sunburn can be harmful.

Missed the Gatekeepers of Governance Summit? Please click here to view the sessions

{kind=link}